Jun 26, 2026Industry Insights

The Impact of U.S. Tariff Increases on China’s Apparel Industry Clusters

How U.S. tariffs impact China’s apparel industry clusters and how major production regions adapt through upgrading, policy support, and global expansion.

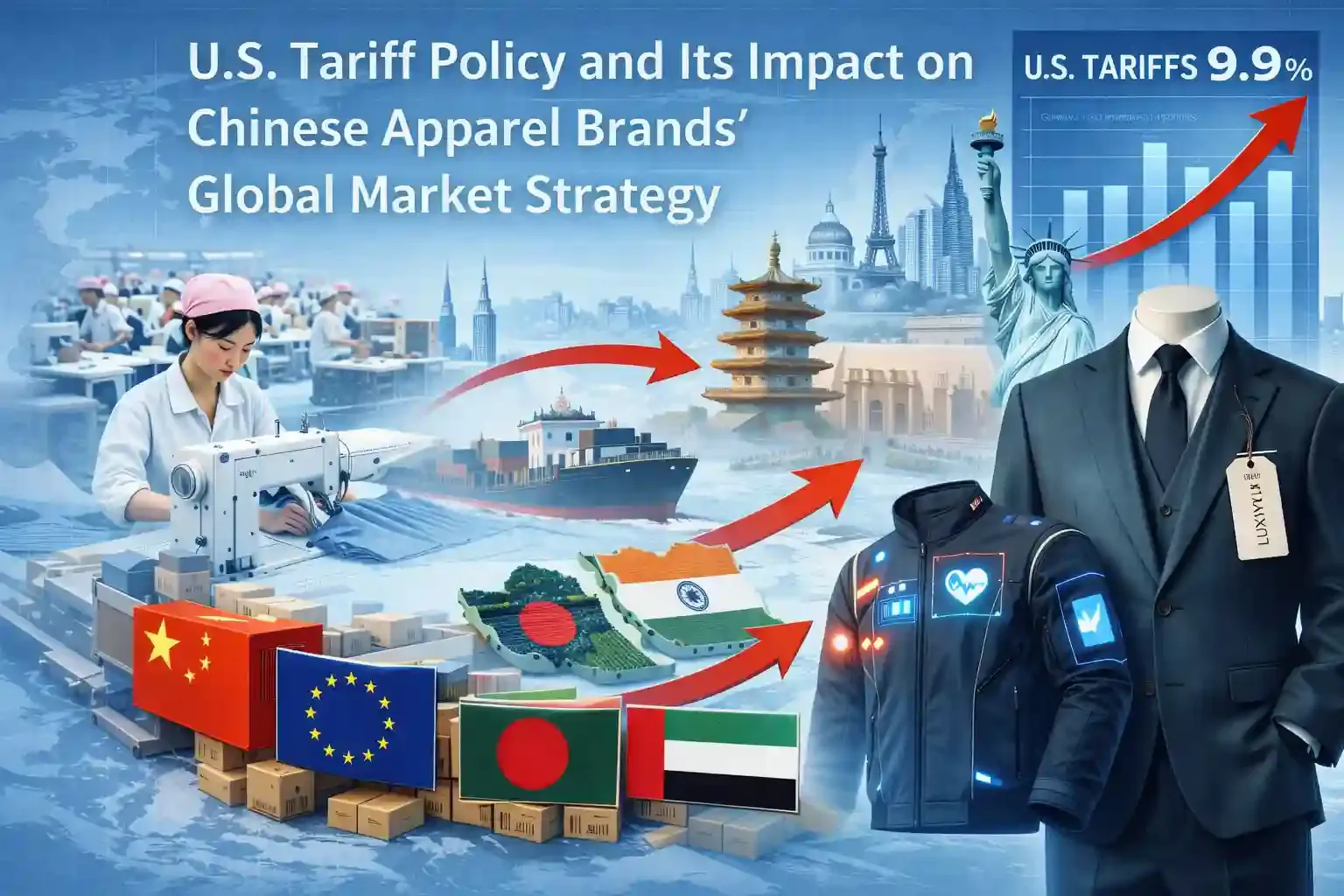

China’s apparel industry has long been built around powerful regional manufacturing clusters. These clusters integrate textile production, garment manufacturing, logistics, and export services within specific geographic regions, creating one of the most efficient apparel supply chains in the world. However, rising U.S. tariffs on Chinese goods have significantly affected these industrial ecosystems.

As of 2026, the pressure created by tariffs has not only influenced individual exporters but has also reshaped the development strategies of China’s major apparel manufacturing clusters.

The Strengths and Challenges of China’s Apparel Industry Clusters

China remains the largest apparel exporter globally. In 2025, China still accounted for roughly 32% of global clothing exports, demonstrating the continued scale and influence of its manufacturing sector.

Much of this production is concentrated in regional clusters. More than 78% of China’s clothing output comes from five provinces: Guangdong, Zhejiang, Jiangsu, Fujian, and Shandong, which form the core of the country’s apparel manufacturing network.

These clusters offer several advantages:

- Integrated supply chains: textile mills, garment factories, accessories suppliers, and logistics providers are located within short distances.

- Specialized production: different regions focus on different product categories such as knitwear, sportswear, or high-end garments.

- Export infrastructure: proximity to major ports like Shanghai, Ningbo, and Shenzhen facilitates global trade.

However, rising U.S. tariffs have created significant challenges for these clusters.

China’s apparel exports experienced noticeable pressure in recent years. In 2025, the country exported about $151.18 billion in garments, while total textile and apparel exports declined about 2.4% year-on-year due to weaker demand and growing competition from other producing countries.

Export prices have also fallen as manufacturers attempt to remain competitive, with the average unit export price of apparel dropping around 8% in 2025.

For many apparel clusters heavily dependent on export markets, especially the United States, this has created increasing economic pressure.

Regional Production Bases Respond to Tariff Pressures

Different apparel clusters across China are responding to tariff challenges in different ways, depending on their industrial structure and market positioning.

Guangdong: The Fast-Fashion Manufacturing Hub

Guangdong, particularly cities such as Guangzhou, Shenzhen, and Dongguan, remains one of the world’s most important fast-fashion manufacturing bases. The region hosts thousands of garment factories serving global fashion brands and retailers.

However, export-oriented factories in the Pearl River Delta have been significantly affected by tariffs and declining orders from Western markets. Some manufacturers have reported shrinking overseas orders and rising operational costs, forcing many small factories to close or shift their focus toward domestic markets and cross-border e-commerce.

To adapt, many Guangdong manufacturers are:

- shifting toward fast-response production models

- strengthening direct-to-consumer e-commerce exports

- investing in automation and flexible manufacturing

Zhejiang: Innovation and Fabric Supply Leadership

Zhejiang Province, including cities such as Hangzhou, Ningbo, and Shaoxing, plays a critical role in textile production and garment design. Shaoxing alone produces billions of garments annually, with a large share exported internationally.

The Keqiao textile market in Shaoxing is one of the world’s largest textile trading hubs, with transaction volumes exceeding $128 billion in 2025.

Faced with tariff pressure, Zhejiang manufacturers are increasingly focusing on:

- higher-value fabrics and technical textiles

- ODM and design-driven manufacturing

- digital fashion supply chains linked to e-commerce platforms

These strategies allow the region to maintain competitiveness despite rising trade barriers.

Jiangsu and Fujian: Upgrading Toward High-Value Production

Jiangsu’s garment industry focuses more on high-quality woven garments, suits, and technical textiles. Meanwhile, Fujian has developed strong capabilities in sportswear manufacturing, particularly around the Jinjiang cluster.

These regions are increasingly investing in:

- advanced textile technology

- sustainable production processes

- global brand partnerships

By moving toward higher-value manufacturing, these clusters aim to reduce dependence on price-driven export markets.

Industrial Cluster Transformation and Global Expansion

The tariff pressures have accelerated structural changes within China’s apparel clusters. Instead of relying solely on low-cost manufacturing, many clusters are moving toward globalized production networks.

A common strategy is the “China + Southeast Asia” supply chain model, where companies maintain design, fabric sourcing, and high-value production in China while relocating labor-intensive processes to countries such as Vietnam, Bangladesh, or Indonesia.

This hybrid model allows companies to:

- reduce tariff exposure

- maintain efficient supply chains

- remain competitive in global markets

At the same time, many clusters are expanding their presence in emerging markets such as Southeast Asia, the Middle East, and Africa to reduce reliance on the U.S. market.

Conclusion

U.S. tariff increases have had a profound impact not only on individual apparel exporters but also on the regional clusters that form the backbone of China’s garment industry. While tariffs have reduced export growth and increased competitive pressure, they have also accelerated the transformation of China’s apparel clusters.

Through technological upgrading, market diversification, and global supply chain restructuring, many Chinese apparel manufacturing regions are adapting to the changing trade environment. These adjustments are likely to reshape the global apparel supply chain over the coming decade.

Despite the challenges, China’s highly integrated industrial clusters continue to provide significant advantages in efficiency, scale, and innovation, ensuring that the country remains a major player in the global apparel industry.